Are you an interest-only mortgage borrower concerned or unsure about how to repay your mortgage at the end of its term? If so, you’re not alone.

This guide outlines the options available which can ensure you are in the best position to settle or repay your mortgage loan when it ends.

What is an interest-only mortgage?

An interest-only mortgage is when the monthly mortgage payments only cover the interest due on the mortgage and not the loan amount itself. This means the original loan amount will not reduce over the term of the mortgage, and will be due to be repaid at the end of the agreed term.

What is a repayment plan?

Borrowers who have an interest-only mortgage need to have a repayment plan in place which will be used to repay the loan amount at the end of its term. Examples of repayment plans are:

-

An endowment policy – an investment product purchased from a life assurance company which is a regular savings plan paying out a lump sum at the end of its term.

-

Stocks and shares (UK) – stocks or shares in a company in which you have invested funds.

-

ISAs – a tax-free savings account with a cap on how much you can save each financial year.

-

Investment bonds – life insurance policies in which a lump sum can be invested in a range of available funds. Some run for a fixed term, others have no investment term.

-

Unit and investment trusts (Open Ended Investment Companies - sometimes known as OEICs) – professionally managed collective investment funds. A fund manager pools money from many investors to buy shares, property or cash assets.

-

Pensions (UK) – a regular payment made by the state or by an employer to people of official retirement age.

-

Sale of second home or other property assets.

-

Sale of the property.

Remember to regularly check your investments as there is always a risk they may underperform and the final value may be insufficient to repay the mortgage loan at the end of its term. This could mean your property would need to be sold to repay what is owed to the lender.

As we are unable to provide advice on investment planning, we strongly recommend you take independent professional advice on this.

Review your payment plan

It is important to regularly check that your repayment plan is still working for you. Here are some steps:

-

Check your original mortgage paperwork to understand when your mortgage term ends and the loan amount that will be outstanding at this time. Ask your lender for further information if you do not have it.

-

When you took out your mortgage, you would have agreed a repayment plan with your lender e.g. using savings, pension/s or selling your property and downsizing (if there was sufficient equity in your property to support this option). Take the time to check what was agreed and if it is still a viable repayment plan. If your repayment plan hasn’t changed and you still have sufficient funds available in your savings, investments, or pensions, you will not need to do anything more.

-

Monitor your accounts on a regular basis to ensure you remain on track to repay your mortgage at the end of its term. If your repayment plan has changed, you may find it difficult to repay your mortgage and there could be a risk of having to sell your home.

-

If you took out an endowment policy to repay your mortgage you should check the investment sum forecasted is sufficient to repay the mortgage at the end of its term. Please note, a number of endowment policies are maturing with significantly lower lump sums than originally forecast. This has created a challenging situation for the homeowners who were relying on the policy to repay their mortgage.

What other options are there to repay your mortgage at the end of its term?

Option one: making monthly or lump sum 'over-payments'

Making over-payments to your mortgage payments will reduce the amount outstanding at the end of its term. For example, paying an additional £25 a month will make a big difference to a mortgage with over 10 years until the mortgage ends.

Option two : switch to a repayment mortgage

You may be able to switch your mortgage from an interest only mortgage to a repayment mortgage (also known as capital and repayment).

There is normally an administration fee to amend your original mortgage contract and your lender may need to check that this change is affordable for you and meets their lending criteria.

This change will increase your monthly mortgage payments, so this option may only be available if you have surplus money left over at the end of each month or you are able to make other financial savings to allow for the increase. However, it will mean you are paying back the capital as well as the interest each month.

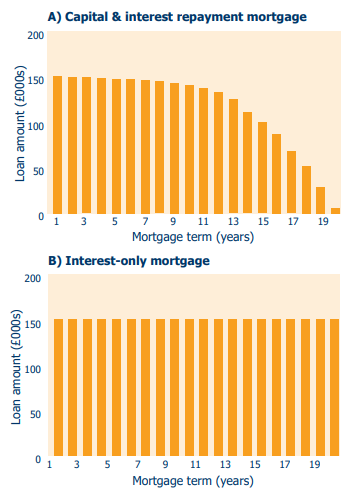

Option 2 example: £150,000 mortgage over 20 years

The graphs below show the mortgage amount outstanding to be repaid at the end of a 20-year term on both interest only and capital and interest repayments.

With a capital and interest repayment mortgage (A) both the capital and interest are paid off over the term of the mortgage and nothing more is owed at the end of the term. With an interest-only mortgage (B), the loan amount does not reduce, and the original loan amount is due at the end of the term.

The interest-only mortgage shows the £150,000 loan amount is the same throughout the term of the loan compared with the capital and interest mortgage which reduces over the term until it is fully repaid.

If you are coming to the end of your mortgage term or your mortgage has already changed to your lender’s standard variable rate, check with your lender to see if you are able to change your mortgage deal to a cheaper rate.

Option three: extend your term

It may be possible for you to extend the term of your mortgage to make it more affordable for you to convert the monthly payments from interest only to capital and interest. This means you will pay back the amount borrowed within the mortgage term.

You may not need to change the whole of your mortgage to capital and interest, especially if you have some savings or an investment in place that may be sufficient to repay part of the mortgage balance.

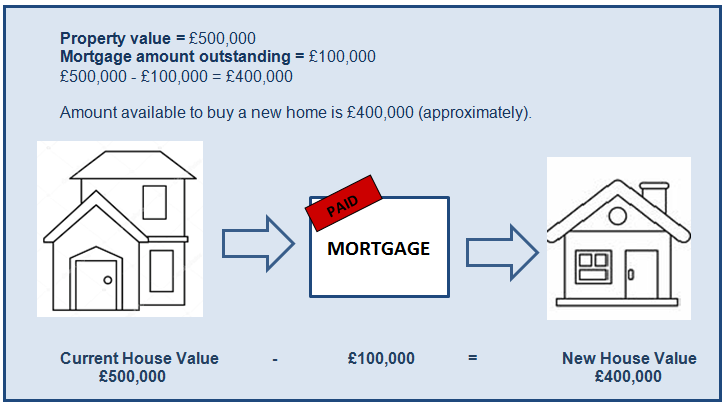

Option four: downsizing

This is where you buy a cheaper property and pay off your outstanding mortgage amount - as shown in the illustration below.

Option four example: downsizing

Remember to consider the costs of moving, for example, estate agent fees and stamp duty, and deduct this from the balance available to buy a new home. You may need to take into account housing market fluctuations and the impact they may have, particularly if house prices decrease.

Keeping track

It is your responsibility to regularly check your repayment plan throughout the life of your mortgage to ensure it is on track. Your lender will contact you at regular intervals to see if your repayment plan is on track and may even ask for you to provide supporting documentation to confirm it.

If your lender thinks your plan is not on track to repay your mortgage at the end of its term, they may contact you to discuss alternative action. This could include switching part or your entire loan to a capital and interest mortgage.

Your lender can help you find an affordable plan to repay your mortgage; the earlier you contact them the more options you will have.

What to do next

-

Check your repayment plan is on track, or if your situation has changed.

-

Contact your lender to discuss which options are available to you.

-

If you are a Newbury Building Society customer our Mortgage Payment Support Team is available on 01635 555588 or you can email our Payment Support Team.

-

Alternatively, you can contact MoneyHelper who provide free, unbiased advice, easy-to-access money tools and information.

-

Read the Financial Conduct Authority’s leaflet ‘Interest-only mortgages: act now and talk to your lender’.